In this blog we will cover the latest RV and travel data news. September 2025 RV production numbers are out, and we’ll cover the latest travel data so you can better gauge if it’s time to buy, sell, or hold an RV. Later, we’ll look at results from a supplier, manufacturer, and large dealer, to see where the industry is at.

RVIA Numbers

On October 27th, 2025, the RVIA posted the latest RV wholesale shipment data for September 2025. Production increased compared to the prior year, with 25,684 total RVs shipped in September, up by 1,098 or 4.4% year-over-year. September 2025 barely passed the lows of 2023 & 2024 shipments but was below all other recent years, all the way back to 2016.

Travel trailer shipments decreased year-over-year, with 17,022 units shipped in September 2025, compared to 17,813 a year ago, representing a decrease of 791 units, or 4.4%. Travel trailers only beat 2023 (the lowest recent year) by a bit more than 500 units.

Motorhome shipments, which include Class A, B, and C motorhomes, were higher than in September 2024, with 2,806 units shipped versus 2,316 a year ago, an increase of just under 500 units or 21% year-over-year. While beating September 2024, Motorhome shipments were still the second lowest on record, going back to 2016.

RV Trader Numbers

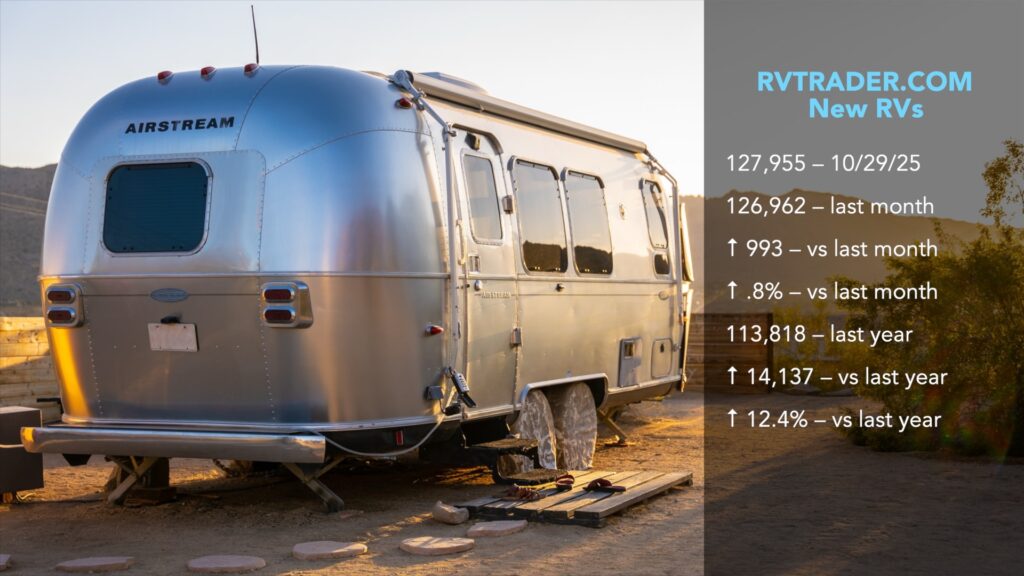

RVs for sale on RVTrader.com have increased since last month, with 127,955 new RVs listed as of October 29th, 2025. This is up from 126,962, or 993 units, or .8% from a month ago, and up 14,137, or 12.4% from a year ago.

The number of used units for sale has increased to another record in the past month at 86,850 used RVs for sale as of October 29th. This is up by 3,620 units, or 4.3%, compared to about a month ago and up by 12,719 units, or 17.2%, compared to a year ago. Used RVs for sale are up over 10,000 since early July indicating a huge unloading after this past camping season.

Model Year Charts

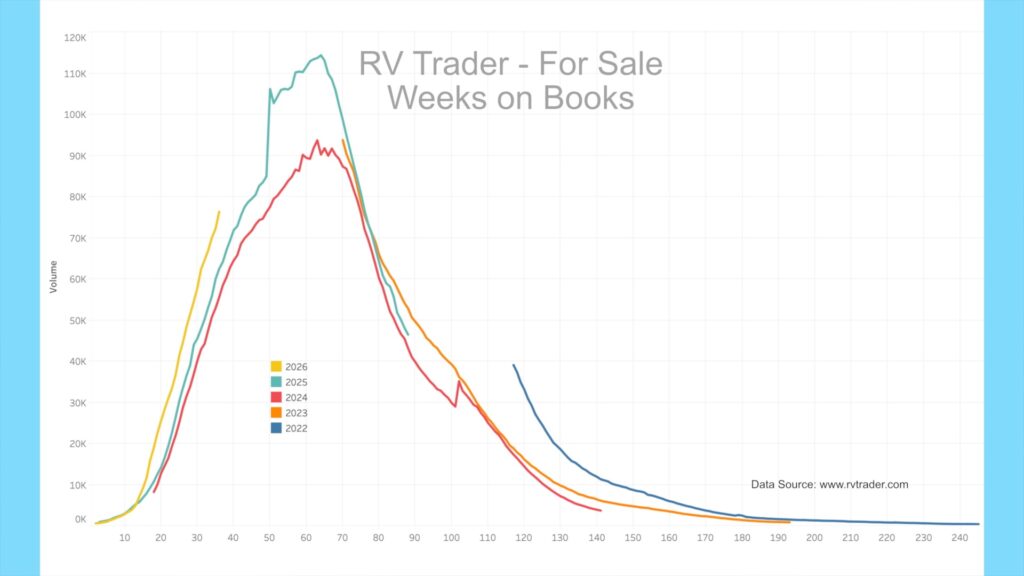

Our model year chart shows new model volumes for 2022 through 2026. The red line shows 2024 models going from 8,238 in late June 2023, ramping up in the spring of 2024, and now at 3,717, down 1,190 or 24% since last month. 2024’s are almost fully run off at this point. 2025 units, as shown by the teal line, have dropped off fast this fall with heavy discounting. I think dealers didn’t want to get caught with too much inventory going into winter, and so pushed to sell 2025s recently. There are currently 46,481 2025 units for sale, decreasing by 11,730 or 20% in the past month. The 2026 models for sale have seen a large increase, with 76,379 units for sale, up by almost 14,000 units or 22.4% since late September.

Over Producing

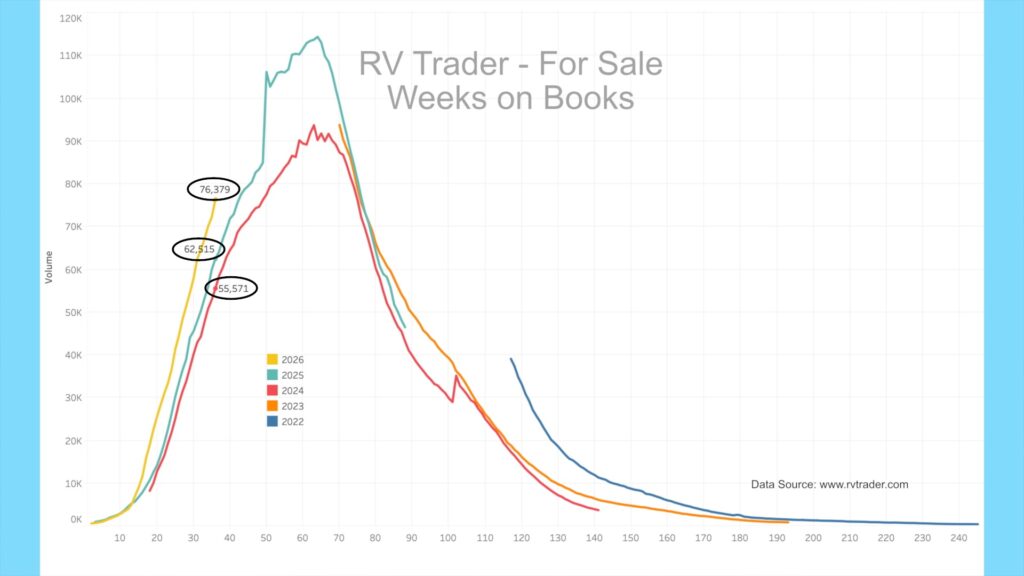

I want to draw attention to the past three model years at the same number of weeks on market—in this case at Week 36 (late October). Week 1 starts late February each year, when we begin to see early signs of the new model year on RV Trader. Notice how each year RV Trader is showing more new units at the same number of weeks on market. For the 2024 models at Week 36, there were 55,571 new units online. For the 2025 models at Week 36, there were 62,515 new units online (+6,944, +12.5%). Looking at the 2026 model run at the same 36 weeks out, there are a whopping 76,379 new units online. This is up 13,864 over the 2025s at the same point last year or 22% more new models for sale at the same point in the calendar!

This is why I think that once again the industry is over-producing. I suppose a combination of early tariff concerns and a bet on lower interest rates moving people back into the market are supporting this decision for dealers to stock up early, driving wholesale deliveries. However, unless buyers come back in droves this spring, many dealers will find themselves with more inventory than even this past season, and heavy discounting will ensue.

As a reminder, many but not all dealers advertise on RVTrader.com to sell inventory. It remains an excellent proxy for overall dealer inventory. You can follow my account on X at @JohnMarucci to receive weekly updates on this data.

AAA

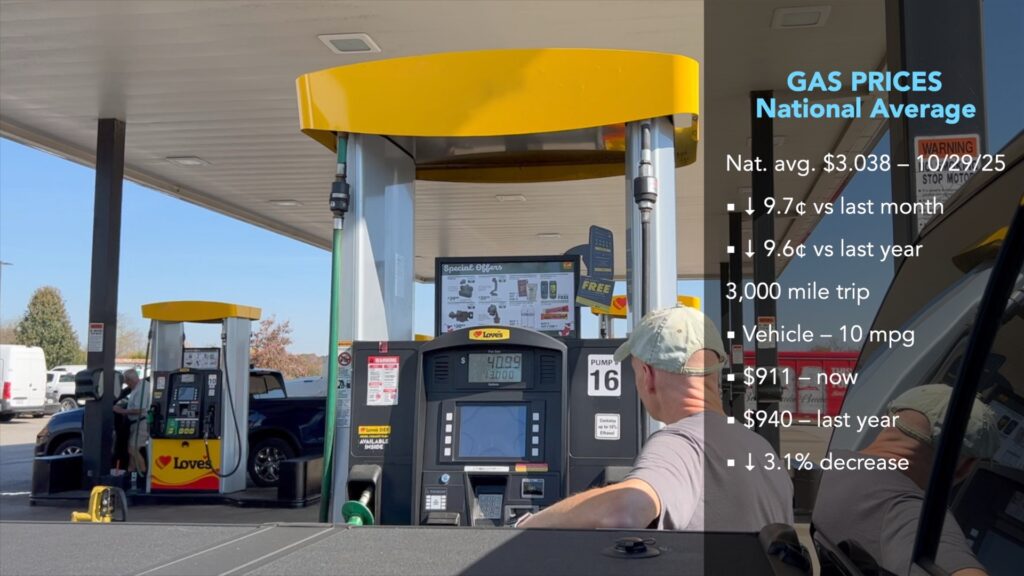

Gas prices have generally declined in the past month. According to AAA, the current average nationwide price as of October 29th was $3.038 per gallon for regular unleaded, down 9.7 cents from a month ago and down 9.6 cents from a year ago. An RV trip of 3,000 miles at 10 mpg would cost $911 now vs. $940 a year ago, a 3.1% decrease. Diesel prices have increased over the past month and currently stand at $3.683 per gallon, up a fraction of a penny versus a month ago and up about 10 cents from a year ago. A similar 3,000-mile trip, getting 12 mpg, would cost $921 now, compared to $894 a year ago, representing a 3.0% increase.

TSA Air Travel Update

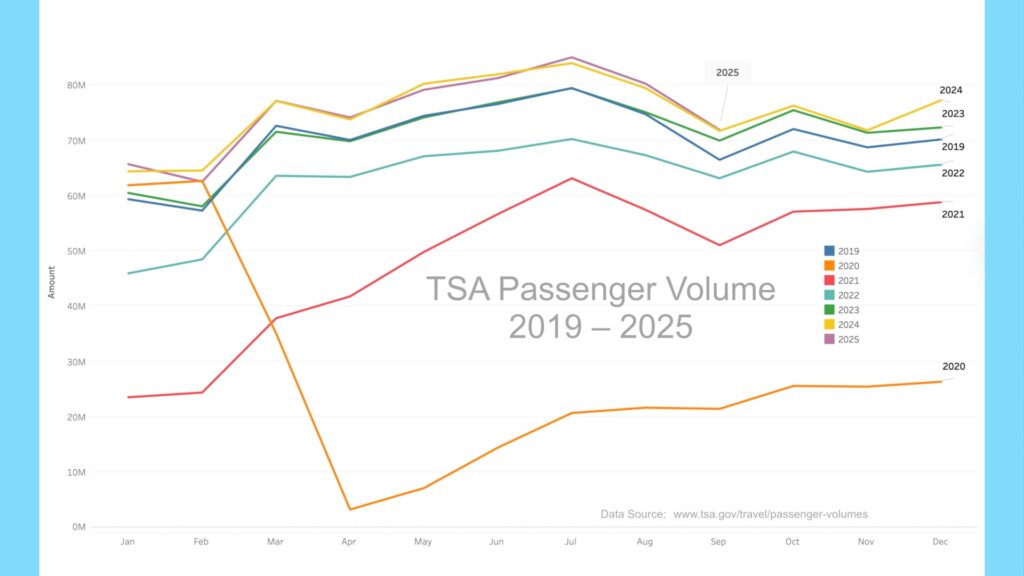

Since the beginning of the pandemic we have tracked the correlation between TSA air travel data and RV shipment data. During the pandemic, air travel tanked while RV shipments took off. The reverse is now true. Air travel is also an indicator of economic conditions. If people stop traveling, it is usually a bad sign for the economy.

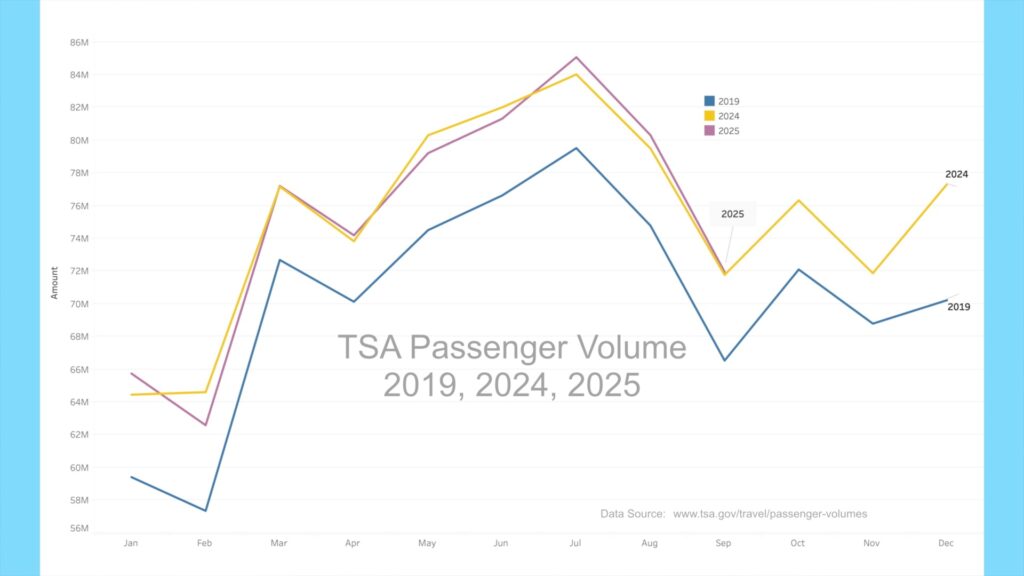

Looking at the latest data from 2019 through September 2025, it is easy to see what happened to air travel. 2020 saw the lowest rates of air travel in the past several years, yet as air travel began to bounce back, the RV industry over-produced. 2019 is the baseline year I was keeping an eye on for air travel numbers to measure against, and as you can see from this chart, it took until August of 2023 for air travel levels to match that of 2019.

Looking at the past two years versus 2019 numbers, we can see that air travel not only rebounded but has been up over 7% each recent year, with 2025 leveling out to 2024 volumes. The average price for an airline ticket in 2019 was $355, in 2024 it was $384 (+8.2%), in 2025 YTD was $392 (+10.4% vs. 2019). The general inflation rate between 2019 and 2024/2025 was 22.8% and 25.5% respectively, so the average airline ticket price costs less now relative to other goods from pre-pandemic levels. So, adjusted for inflation, air travel is cheaper now than in 2019. I think this is one reason the RV industry has had to downgrade production estimates regularly.

Earnings

It’s earning season again and we can glean insight on how things are going with the industry by looking at results from the larger publicly traded manufacturers, wholesalers, and large dealers.

Dometic

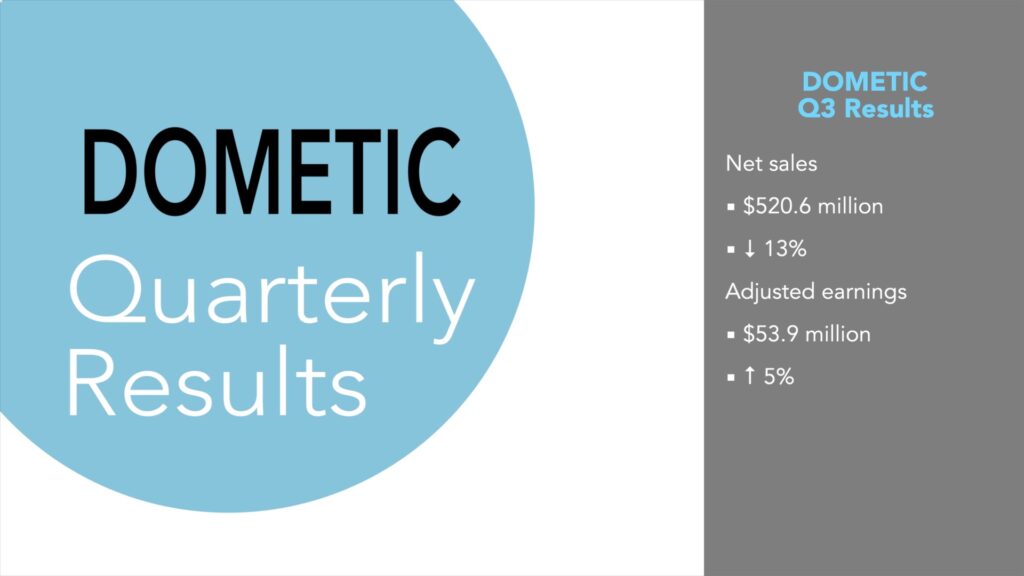

Dometic Group, a major supplier for North American RVs, reported its Q3 2025 results on October 23, showing resilience amid macroeconomic headwinds and cautious consumer spending. Net sales fell to $520.6 million, down 13%, driven by volume declines across segments, but adjusted earnings before taxes rose to $53.9 million, up 5%, through cost savings and restructuring. CEO Juan Vargues noted early stabilization in orders, positioning the company for recovery as interest rate cuts potentially lift demand in RV and marine markets.

Translation: sales of components for RVs has softened, and Dometic has had to cut costs to combat the sales shortfall. It seems that Dometic products are showing up less and less in new RVs. My take is that quality issues have been problematic with Dometic items and manufacturers have somewhat grown weary of warranty issue. GE air conditioners, Furrion fridges (made by Lippert), and Truma products seem more evident in many newer RVs. If this is the case, Dometic is losing market share more permanently and a turn-around in RV sales won’t help all that much.

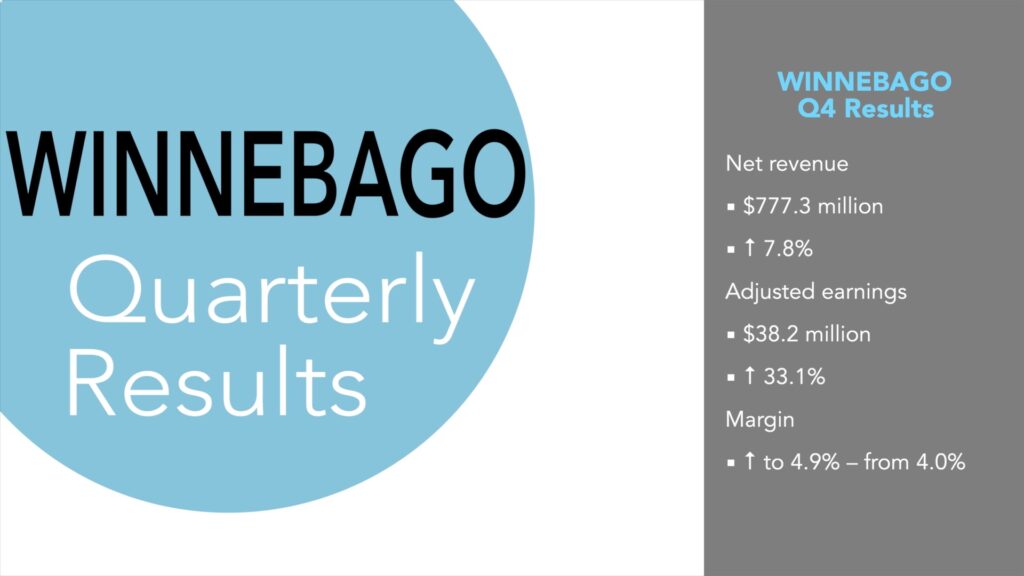

Winnebago

Winnebago Industries reported its Q4 FY2025 results on October 22, showing resilience amid RV market challenges and inventory destocking. Net revenues rose to $777.3 million, or 7.8%, driven by favorable product mix and price increases, while adjusted earnings before taxes climbed to $38.2 million, or 33.1%, boosting the margin to 4.9% from 4.0% through operational efficiencies and segment gains. CEO Michael Happe highlighted solid revenue growth, improved profitability, and positive new product momentum, positioning the company for enhanced margins and efficiency as mid-cycle demand recovery unfolds.

Translation: Winnebago weathered a big storm with the Grand Design frame flex fiasco and is pretty much past it at this point. They have had to cut costs to account for lower overall sales but are starting to rebound. Winnebago has been a strong brand with good mid-level pricing and innovation.

CEO Michael Happe commented, “While industry conditions continue to reflect higher competitive discounts and allowances, we remain disciplined in how we manage production schedules and inventory levels. Our focus on aligning our shipments with retail demand has positioned us well to support our dealer partners, maintain inventory health, and keep our brands strong in the eyes of consumers.” This means Winnebago is trying hard to not overproduce, which is key to seeing prices stay firm. I like this approach, as manufacturing discipline should mean higher average line tenures on the factory floor and better quality for the end user.

Camping World

On October 28th, Camping World posted third quarter fiscal results. Revenue reached $1.80 billion, marking a 4.7% increase or $81.1 million year-over-year, primarily driven by a robust 31.7% surge in used vehicle revenue that offset a 7.0% decline in new vehicle sales. The average selling price of new vehicles decreased by 8.6% year-over-year. More of the company’s sales are coming from used vehicles, with 18,694 units sold and revenue increasing by 33%. While the average selling price of new units declined by 8.6%, the average selling price of used units decreased by less than 1%. So, 48.6% of Camping World’s unit sales now come from used units with higher margins.

Camping World has moved toward using used RVs as a primary driver of sales, given margins are higher and average price is lower. The average selling price of a new RV at Camping World was $37,798, while the average selling price for a used RV was $31,512.

CEO Marcus Lemonis spoke to 2026 expectations, “we are extremely confident in our ability to once again outperform the RV industry, grow our earnings, and continue to reduce our leverage year-over-year. As expected, affordability is still top of mind for consumers, and rising prices could create resistance on demand. This is leading us to deliberately set conservative new volume growth assumptions.” This shows an expected cautious outlook for the coming year from the largest RV dealer.

My Take

Given the lower average price, it seems Camping World is understanding the price sensitivity of buyers right now and acting to accommodate by stocking more used models. That being said, it seems apparent that new RVs, especially 2025 models, are being discounted much more this year than 2024s were at the same time last year. A 9% lower actual discounted price on new RVs a year later speaks to the glut of 2025s produced that we have spoken to many times. It also begs the question of purchasing a new 2025 on the lot. New units are only about 20% more on average than used units right now. If this gap continues to shrink, I think we will see new unit sales pick up in the new year.

Meanwhile if you are in the market for a new RV, it may not be a bad to time begin a search this fall, especially on remaining discounted new 2025 models. There are still pricing and quality concerns, however, I see this as the best buying opportunity we have had in several years.

That should do it. All the best in your camping adventures!

As always, thanks to our fans who support our efforts by starting their shopping from our Amazon Storefront and their generous financial support by using the THANKS feature located under each YouTube video ($ within the Heart icon). Your support is greatly appreciated!